At the time of the publication of the 2019 budget law on 29 April 2019, a Grand Ducal Regulation of 26 April 2019 was published. This Regulation amends the Appendix A and B determining the limits and conditions for the application of the reduced and super-reduced VAT rates.

As from 1st May 2019, following VAT rates changes are applicable:

- electronic publications (3% instead of 17%),

- essential hygienic items (3% instead 17%) and

- plant protection products for organic culture (8% instead of 17%).

In our previous VAT newsletter, we mentioned that some uncertainties remained especially as regards as the qualification of certain publications as electronic publications (e.g. for audio book).

The VAT authorities issued the circular 753 (Circulaire N° 793 du 17 mai 2019) on 17 may 2019 that contains clarification on the following topics:

- the criteria to take into consideration in order to apply the new VAT rate;

- which kind of products are covered by these new measures (especially regarding the qualification of electronic publications

1. Taxable event / chargeability of VAT

The VAT rate applicable is the one that became effective as from the date of the entry into force of the new regulation (I.e. as from 1st May 2019).

However, the circular reminds that the rate applicable to the supply of goods and the supply of services is the one that is into force when the taxable event takes place. This is common practice to clarify as from when the new VAT rates are applicable. Thus, the following has to be taken into consideration:

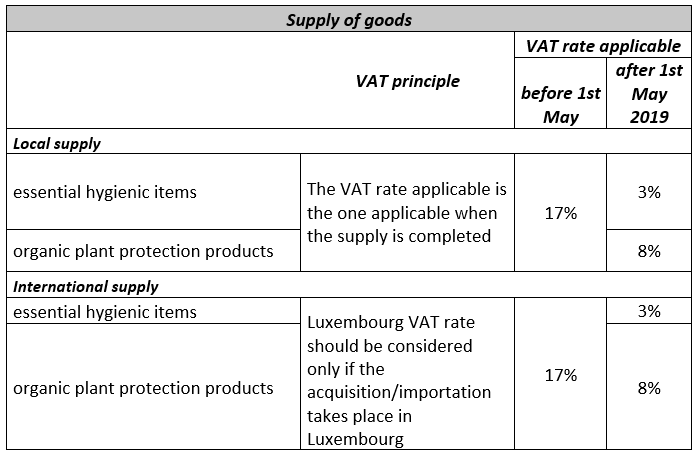

- Supply of goods (essential hygienic items / organic plant protection products)

- Local supply: the VAT rate applicable is the one applicable when the supply is completed

- International supply : Luxembourg VAT rate should be considered only if the acquisition/importation takes place in Luxembourg

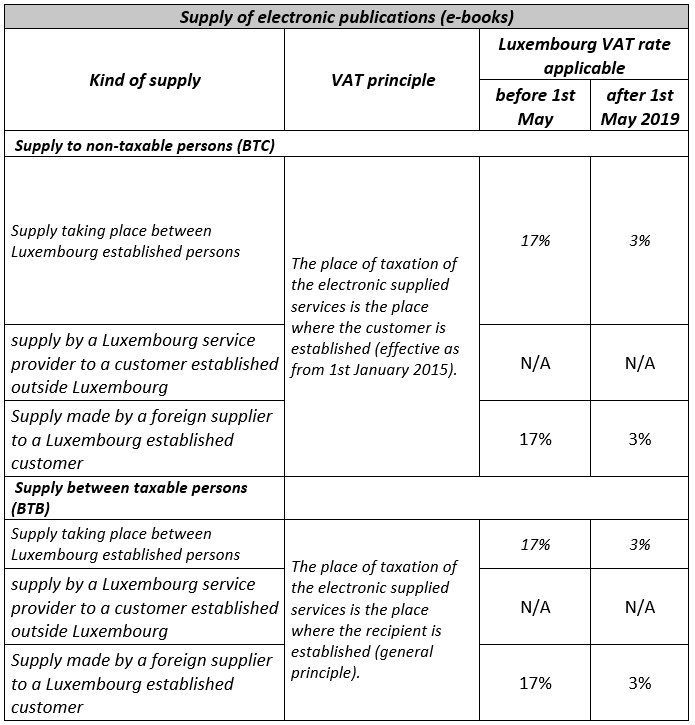

- Supply of electronic services (electronic publications)

Exceptionally, these will not apply to :

- Advance payment

Tax is due in principle on the date of receipt of the payment (this measure does not apply to cross-border transactions)

- If the issuance of an invoice is mandatory (as this is mostly the cases), the tax is due on the date of issuance of the invoice that should be issued no later than the 15th of the month following the completion of the supply.

Finally the circular also mentions that the goods that need to be assembled or transformed (work under contract - travail à façon), benefits from the VAT rate applicable at the time of the completion of the work.

The date of issuance of the invoice issued within the legal deadline should be the major criteria to take into consideration to determine which VAT rate is applicable to the supply of goods / supply of services.

We can help Luxembourg companies by reviewing their flows of transactions to monitor the VAT obligations in Luxembourg.

2. Goods within/out of the scope

2.1 Electronic publications taxable at the super-reduced rate

The circular recalls the definition of books that are eligible to the super-reduced rate relying on their customs classification (Customs Nomenclature “CN” 4901, 9706, 4902, 4903, 4904, 4905, 4505 91) and mentions that the download of a digital file is a supply of services that is not subject to CN classification (contrary to the paper format).

It mentions that the following publications are excluded from the application of the super-reduced rate:

- Publications dedicated exclusively or mainly to advertising

- Publications fully or mainly containing video or audible music;

- Publications with fully or mainly pornographic content

a) Exclusion of publications dedicated exclusively or mainly to advertising

This reasoning is based on the court case C-390/15 RPO, where the court stated that the objective underlying the application of a reduced rate of VAT to the supply of books consists in the promotion of reading. This explains the exclusion of advertising publications that do not meet this objective, such as:

- brochures,

- flyer,

- commercial catalogues,

- tourist publicity.

b) Exclusion of publications fully or mainly containing video or audible music

Exclusion of publications fully or mainly containing video or audible music is justified by the wording “books, brochures and similar printouts” which is the definition of printed book. It follows that any supply must result in a reproduction of the same information content as the printed books. However, a publication fully or mainly containing video or music does not fulfil this criterion essentially if the content is of decisive importance for the purchaser and is an end in itself. Any literary content of such publication should be seen as accessory.

c) Exclusion of publications with fully or mainly pornographic content

On one hand are excluded from the application of super-reduced rate any material consisting fully or predominantly in pornographic content and on the other hand publications consisting wholly or predominantly in video content or audible music, whether provided on physical or electronic format.

2.1.1 Library

The application of the super-reduced rate also applies, in this context to the following transactions, provided that the publications concerned would benefit from the application of the super-reduced rate if they where supplied against consideration:

- Rental against consideration of publications made available in a library on any format (physical or electronic),

- Subscriptions or bouquets of subscriptions against consideration allowing access to publications on any format (physical and/ or electronic).

3) Essential hygienic items

In principle, all hygienic protection devices intended to respond to menstrual losses may benefit from the application of the super-reduced rate (e.g. CN 9619 / CN 3926 90 97 / CN 0511 99 31 / CN 0511 99 39).

4) Plant protection products for organic culture

The reduced rate applies, as from 1 May 2019, to plant protection products authorized in organic farming by the competent administration “l’Administration des services techniques de l’agriculture”” (ASTA). Such authorization may be granted if the requirements laid down in the amended Council Regulation (EC) No 834/2007 of 282007 on organic production and labelling of organic products are complied with.

A list of products to the delivery of which the reduced rate may apply is available online on the web site of ASTA.

Sylvie Eiras de Sa - Senior Associate (sylvie.eiras@tiberghien.com)